Aging in place vs. assisted living cost comparison starts with a clear question: what does it actually cost for an older adult to remain safely at home, and when does assisted living become the more practical financial choice? Aging in place means staying in one’s current home while adapting routines, support, and the physical environment to match changing mobility, health, and daily living needs. Assisted living is a residential option that combines housing, meals, personal care, social programming, and varying levels of supervision in one monthly fee. Families often compare these paths only after a fall, hospital discharge, or dementia diagnosis, but the smartest planning starts earlier, when there is still time to evaluate home safety, budget realistically, and choose upgrades that preserve independence.

I have worked with families making this decision after orthopedic surgeries, progressive neurological diagnoses, and ordinary age-related decline, and the same mistake appears repeatedly: they compare a rent payment at an assisted living community to a mortgage payment at home and assume home is automatically cheaper. That is rarely an apples-to-apples comparison. A true cost comparison must include home modifications, caregiving hours, transportation, meal preparation, maintenance, utilities, and the hidden economic impact on adult children who start filling unpaid care gaps. It also must account for care intensity. A home that works well for a healthy 72-year-old may become expensive and risky for an 84-year-old who needs help with transfers, toileting, medication reminders, and overnight monitoring.

This guide explains aging in place strategies as a complete planning framework, not just a checklist of grab bars and ramps. You will see how to estimate costs, identify the main drivers of spending, and match care needs to the most sustainable living arrangement. As the hub page for aging in place strategies within accessibility and mobility solutions, it also covers the key decisions that connect to wider topics such as bathroom accessibility, stair solutions, transfer equipment, mobility aids, and smart home monitoring. The goal is practical clarity: understand the numbers, recognize the tipping points, and make a decision that protects both safety and long-term financial stability.

What aging in place really includes

Aging in place is often described as staying at home, but in practice it is a layered support model. It combines accessible design, assistive technology, preventive health management, transportation planning, and either informal or paid caregiving. For independent older adults, the strategy may center on lighting improvements, a no-step entry, lever door handles, medication organization, and rides to appointments. For someone with arthritis, Parkinson’s disease, stroke recovery, or early dementia, the plan becomes broader and more expensive, often involving shower conversions, bed mobility aids, personal care assistance, and monitoring systems.

The most effective aging in place strategies begin with function, not with products. Occupational therapists frequently assess activities of daily living such as bathing, dressing, transferring, toileting, eating, and mobility. They also evaluate instrumental activities like cooking, shopping, managing medications, and handling finances. That distinction matters because a person may look independent to relatives who visit briefly while quietly struggling with bathing or meal preparation every day. Once those deficits appear, families either spend money on home adaptation and support services or shift the person into a setting where those services are already built into the monthly fee.

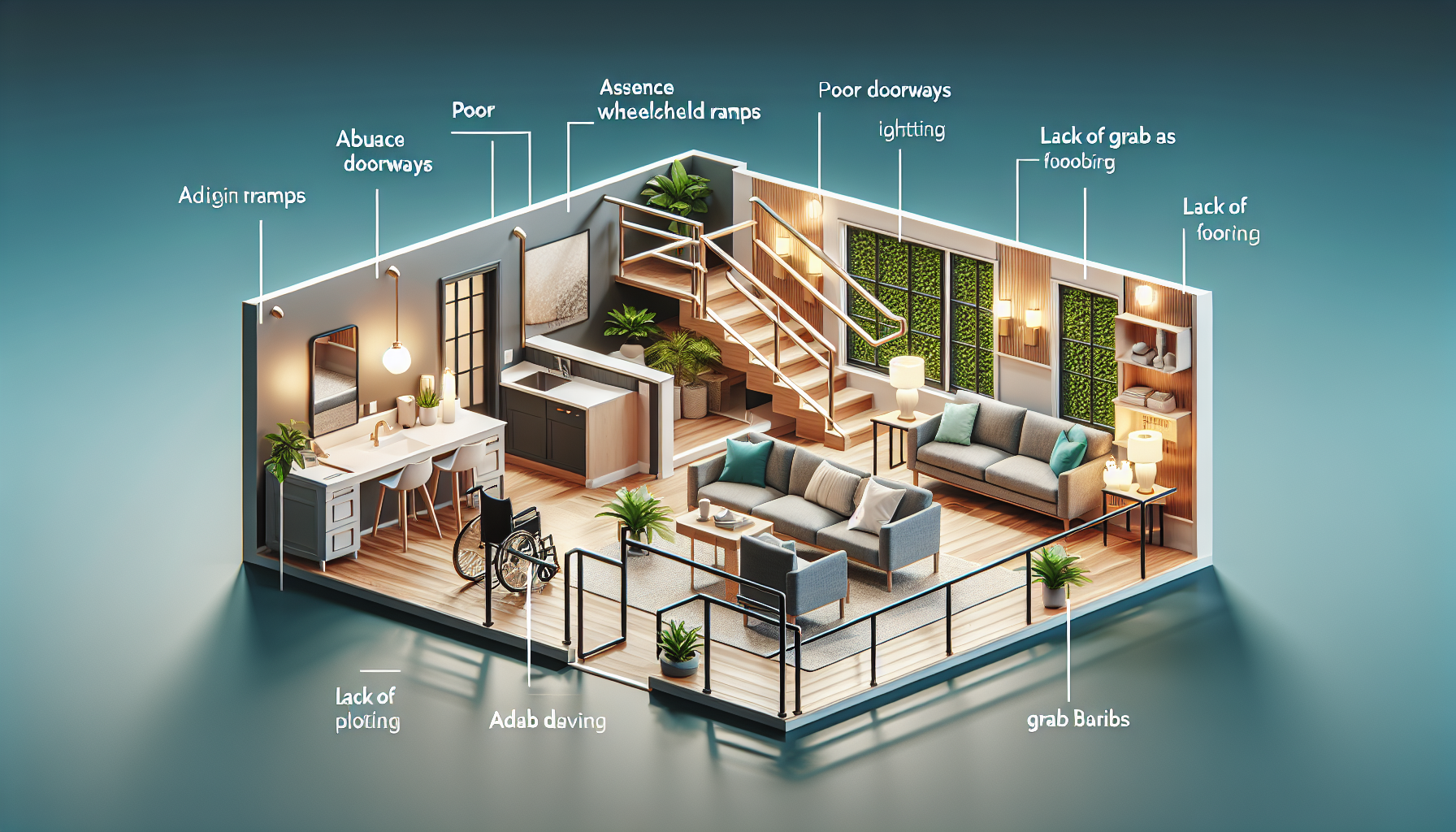

Home modifications range from low-cost fixes to major renovations. Common upgrades include grab bars, raised toilet seats, handheld showerheads, non-slip flooring, improved task lighting, widened doorways, threshold removal, ramps, stair lifts, and first-floor bedroom conversions. The Centers for Disease Control and Prevention consistently identifies falls as a major source of injury among older adults, so preventing slips and transfer accidents is not optional. A well-designed home can reduce hospitalization risk, preserve confidence, and delay institutional care. But every modification must fit the person’s diagnosis, gait pattern, cognition, and expected progression, or money gets spent on equipment that is poorly used.

How assisted living pricing works

Assisted living pricing is simpler on the surface and more variable underneath. Most communities charge a base monthly rate covering housing, utilities, meals, housekeeping, social activities, and some level of staff availability. On top of that base, many add care tiers for help with bathing, dressing, medication administration, transfers, incontinence support, or memory-related supervision. National median figures published by Genworth’s Cost of Care Survey place assisted living around the mid-$5,000s per month in recent years, but local rates can be far higher in major metro areas or lower in smaller markets. Entrance fees are uncommon compared with continuing care retirement communities, yet move-in fees, community fees, and annual rate increases are common.

Families should ask for a full fee schedule, not just the advertised monthly price. I have seen communities market an attractive base rate that excludes medication management, shower assistance, escorting to meals, incontinence supplies, and additional transfer support. Within six months, the resident’s bill can look very different. On the other hand, assisted living can absorb costs that are fragmented and difficult to manage at home. Meals are centralized, transportation may be scheduled, socialization is built in, and emergency response is immediate. For older adults living alone, that bundled structure can reduce crisis spending caused by malnutrition, missed medications, isolation, or delayed treatment after a fall.

Another pricing reality is level-of-care creep. If an older adult begins in assisted living with minimal support but later requires two-person transfers, extensive wandering supervision, or skilled nursing, the community may raise the care tier or require a move to memory care or nursing care. That means assisted living is not a fixed final cost. It is a stage on a continuum. Still, compared with patching together twenty or thirty weekly hours of home care, it often provides more predictability, especially for families who live at a distance and cannot coordinate multiple providers.

Direct cost comparison: home versus community living

A meaningful aging in place vs. assisted living cost comparison has to separate one-time costs from recurring monthly costs. One-time home expenses might include a ramp, bathroom remodel, stair lift, or hospital bed. Recurring costs can include home care aides, meal delivery, housekeeping, lawn care, transportation, remote monitoring subscriptions, and higher utility usage because the person is home all day. Assisted living usually shifts many of those line items into one recurring bill, but may still leave out pharmacy delivery, continence supplies, salon services, and external medical appointments.

| Cost Category | Aging in Place | Assisted Living |

|---|---|---|

| Housing | Mortgage, rent, taxes, insurance, maintenance | Included in monthly community fee |

| Meals | Groceries, meal prep help, delivery services | Usually included |

| Personal care | Hourly home care, often rising with need | Often tiered add-on or partly included |

| Accessibility | Home modifications and equipment purchases | Built environment already accessible |

| Transportation | Rideshare, family time, paratransit, fuel | Often scheduled transportation included |

| Social support | External senior centers or private programs | Activities usually included |

Consider a practical example. An older homeowner with a paid-off house may spend $1,200 monthly on taxes, insurance, utilities, groceries, maintenance reserves, and internet before any care begins. Add twenty hours a week of nonmedical home care at $30 per hour, and monthly care alone is roughly $2,600. Add housekeeping, transportation, and meal support, and the real monthly total can approach or exceed $4,500 without counting future repairs. If care rises to forty hours a week, the home care portion doubles. Once overnight coverage becomes necessary, aging in place becomes dramatically more expensive than many assisted living communities.

Now consider a person entering assisted living at $5,500 per month with one care tier adding $800. That total may be higher than living at home with minimal support, but lower than staying home with frequent aide visits, extensive family coordination, and recurring home upkeep. The crossover point differs by region and by health status, yet the pattern is consistent: aging in place is usually less expensive when the older adult is largely independent and the home needs modest modifications. Assisted living often becomes financially competitive when supervision or hands-on care is needed every day.

The biggest cost drivers families miss

The first missed driver is unpaid family labor. Daughters, sons, and spouses often provide transportation, medication setup, grocery shopping, technology troubleshooting, appointment coordination, laundry, and safety checks. Economically, that time has value even if no invoice is issued. When an adult child reduces work hours, takes unpaid leave, or travels constantly to manage crises, the household cost of aging in place rises sharply. Families should count this burden honestly. If the plan works only because one relative is exhausted, the plan is unstable.

The second driver is home suitability. A single-story condo with an accessible shower is very different from a two-story house with narrow bathrooms and multiple entry steps. Structural changes can be costly, especially when plumbing must be moved for a curbless shower or doorways need widening for walker and wheelchair clearance. The third driver is medical complexity. Diabetes, heart failure, cognitive decline, and fall history all increase supervision needs. A person who forgets to lock doors or take medications may need much more support than someone with the same physical mobility limitations but intact executive function.

The fourth driver is isolation. I have seen older adults remain at home safely on paper while deteriorating because they stopped cooking, moved less, and withdrew socially. Loneliness can drive depression, poor nutrition, and avoidable hospital use. Assisted living does not solve every emotional problem, but it can remove logistical barriers to activity and routine. The fifth driver is emergency response time. At home, a fall at 2 a.m. may leave someone on the floor for hours unless monitoring is in place. In a staffed setting, help usually arrives much faster. That difference affects not only quality of life but also downstream medical spending.

Best aging in place strategies to control cost and risk

The best aging in place strategies focus on prevention before crisis. Start with a home safety assessment by an occupational therapist, certified aging-in-place specialist, or experienced accessibility contractor. Prioritize high-impact changes: remove trip hazards, improve lighting, install secure handrails, add grab bars anchored correctly, and address bathroom transfers. These are relatively affordable compared with hospitalization after a fall. If stairs are becoming unsafe, compare the long-term cost of a stair lift against first-floor relocation within the home. Do not assume the most visible solution is the best one; many households do better by relocating sleeping and bathing functions downstairs.

Next, build a care plan in stages. Use the lightest effective support first: medication organizers, automatic dispensers, grocery delivery, housekeeping help, transportation services, and adult day programs. Expand to personal care assistance only as needed. This staged approach often preserves cash flow better than jumping immediately into broad private-duty coverage. Technology helps too. Video doorbells, fall detection wearables, smart speakers, stove shutoff devices, and remote patient monitoring can reduce risk, but they are supplements, not substitutes, for human oversight when cognition is declining.

Financial planning should include funding sources and limits. Medicare generally does not pay for long-term custodial care. Medicaid may help with long-term services in some states, often through waiver programs, but eligibility rules are strict. Long-term care insurance can offset home care or assisted living costs if a policy is in force and benefit triggers are met. Veterans may qualify for Aid and Attendance benefits. Families should also review tax implications, home equity, and whether a reverse mortgage is appropriate. The right strategy is the one that can be sustained for years, not just the next three months.

When assisted living is the better value

Assisted living is the better value when daily support needs are regular, socialization is poor at home, and the family system cannot provide reliable backup. It is also often the better value when an older adult lives alone with mild cognitive impairment, increasing frailty, or repeated falls. In those situations, the monthly community fee buys more than room and board; it buys routine observation, easier access to help, structured meals, and a built environment designed for older bodies. That combination can reduce preventable crises and relieve caregiver burnout.

There are limits. Assisted living is not the right fit for everyone, especially people who need skilled nursing around the clock or who strongly resist communal settings. Yet families should not frame the move as a failure of independence. In many cases, it is a strategy for preserving functional independence longer by reducing the friction and risk of living alone in an unsuitable home. The best next step is simple: calculate your true monthly home cost, assess the home for safety, compare it with local assisted living pricing, and make the decision before a crisis makes it for you.

Frequently Asked Questions

What costs should families include when comparing aging in place to assisted living?

Families should look beyond the most obvious monthly bills and compare the full cost of daily living in both settings. For aging in place, that usually starts with housing expenses such as mortgage or rent, property taxes, homeowners insurance, utilities, internet, maintenance, lawn care, snow removal, and housekeeping. Then come the support-related costs that often grow over time, including home health aides, personal care assistance, medication management, meal delivery, transportation, adult day programs, and private duty care. Many households also need to factor in one-time or periodic home modifications like grab bars, ramps, stair lifts, walk-in showers, improved lighting, widened doorways, or medical alert systems. On top of that, healthcare-related expenses may increase if frequent appointments, hospital follow-up, or in-home skilled services become necessary.

Assisted living typically bundles many daily living costs into a monthly fee, which can make comparison easier but still requires a close read. Common charges include room or apartment rent, meals, housekeeping, laundry, social activities, staff oversight, and some level of personal care. However, many communities also use tiered pricing or add-on fees for help with bathing, dressing, medication administration, continence care, escort services, or higher levels of supervision. To make a fair comparison, families should calculate current monthly spending, identify which costs are likely to rise over the next one to three years, and ask whether unpaid family caregiving is covering a real financial gap. A realistic comparison is not just home versus facility rent; it is total cost of safe, sustainable daily living.

Is aging in place usually cheaper than assisted living?

Aging in place can be cheaper in some situations, but it is not automatically the lower-cost option. It tends to be more affordable when the older adult is relatively independent, already lives in a paid-off or low-cost home, and only needs limited support such as occasional housekeeping, meal help, or a few hours of caregiving each week. In those cases, staying home may preserve routines, reduce disruption, and keep monthly expenses lower than a residential care setting. This is especially true if major home repairs are not needed and family members are able to assist with transportation, errands, or daily check-ins.

That picture can change quickly as care needs increase. Once an older adult begins needing daily personal care, regular supervision, medication reminders, mobility help, or coverage across evenings and weekends, the cost of patching together in-home support often rises sharply. Hiring caregivers for multiple hours a day, seven days a week, can exceed the monthly price of assisted living in many markets. In addition, homeownership brings unpredictable costs such as roof repairs, plumbing issues, appliance replacement, and accessibility upgrades. Assisted living may become the better financial value when it replaces several separate expenses at once: housing, meals, social engagement, transportation, and a baseline level of care. The most accurate answer depends on the person’s care needs, local labor rates, and whether the home environment can remain safe without extensive spending.

At what point does assisted living become the more practical financial choice?

Assisted living often becomes the more practical financial choice when care needs become consistent rather than occasional. A useful tipping point is when the older adult needs daily help with multiple activities of daily living, such as bathing, dressing, toileting, transferring, or medication management, and that help can no longer be covered reliably by family alone. Another sign is when support at home requires multiple paid services layered together, such as housekeeping, meal delivery, transportation, personal care aides, and home safety technology. Once those services start overlapping, the monthly total may approach or exceed assisted living fees without providing the same level of coordination or built-in oversight.

Financial practicality is also about predictability and sustainability, not just the lowest immediate number. Assisted living can simplify budgeting because many essential services are centralized under one provider, and emergency planning is often built into the environment. Families should also consider indirect costs that are easy to overlook, including lost work hours for adult children, caregiver burnout, last-minute schedule gaps, repeated hospital discharges, and the need for urgent home changes after a fall or health event. If staying at home requires constant problem-solving, escalating spending, and heavy dependence on unpaid caregivers, assisted living may offer not only operational convenience but also a clearer and more manageable long-term financial plan.

How do home modifications and safety upgrades affect the cost comparison?

Home modifications can significantly influence whether aging in place remains affordable. Some upgrades are relatively modest, such as grab bars, non-slip flooring, brighter lighting, lever-style door handles, raised toilet seats, or handheld shower heads. Others are much more expensive, including stair lifts, wheelchair ramps, bathroom remodels, widened hallways, first-floor bedroom conversions, exterior entry changes, or kitchen redesigns for limited mobility. These costs may be one-time expenses, but they can be substantial, particularly in older homes that were never designed for accessibility. Families should also remember that modifications do not eliminate the need for care; they make the home safer, but they do not replace supervision, transportation, meal support, or hands-on assistance.

That said, modifications can still be financially smart if they extend independence and reduce the need for more expensive services. For example, a safer bathroom or better home access may prevent falls, delay a move, and lower the amount of caregiving needed in the short term. The key is to match the investment to the expected benefit. Spending a moderate amount to improve safety may make excellent sense for someone with stable needs, while a major remodel may be harder to justify if health changes suggest a move to assisted living is likely in the near future. Families should compare the upfront cost of modifications, the ongoing cost of in-home support, and the probable timeline for future care needs rather than evaluating upgrades in isolation.

What is the best way to make a realistic month-to-month cost comparison?

The best approach is to build a side-by-side monthly budget using actual numbers, not estimates based on assumptions. Start with current household expenses for living at home: mortgage or rent, taxes, insurance, utilities, groceries, home maintenance, transportation, cleaning, and technology. Then add support costs that are already in place or likely to be needed soon, such as companion care, personal care aides, medication management, meal delivery, physical therapy, adult day services, and emergency response systems. If the older adult relies heavily on family members, assign a realistic value to that time as well, even if no money is currently changing hands. This helps reveal the true resource burden of remaining at home.

Next, collect detailed pricing from assisted living communities, including base rent, care level fees, community fees, medication services, transportation policies, and what is included in meals, housekeeping, and activities. Ask specifically how costs increase if the resident needs more help later, because the entry-level price may not reflect future reality. Once both monthly profiles are built, compare not only today’s total but also likely six-month and twelve-month scenarios. A realistic cost comparison should answer three questions: what is affordable now, what remains sustainable as needs increase, and which option provides the safest and most dependable support for the money being spent. That broader view leads to better decisions than focusing on headline prices alone.